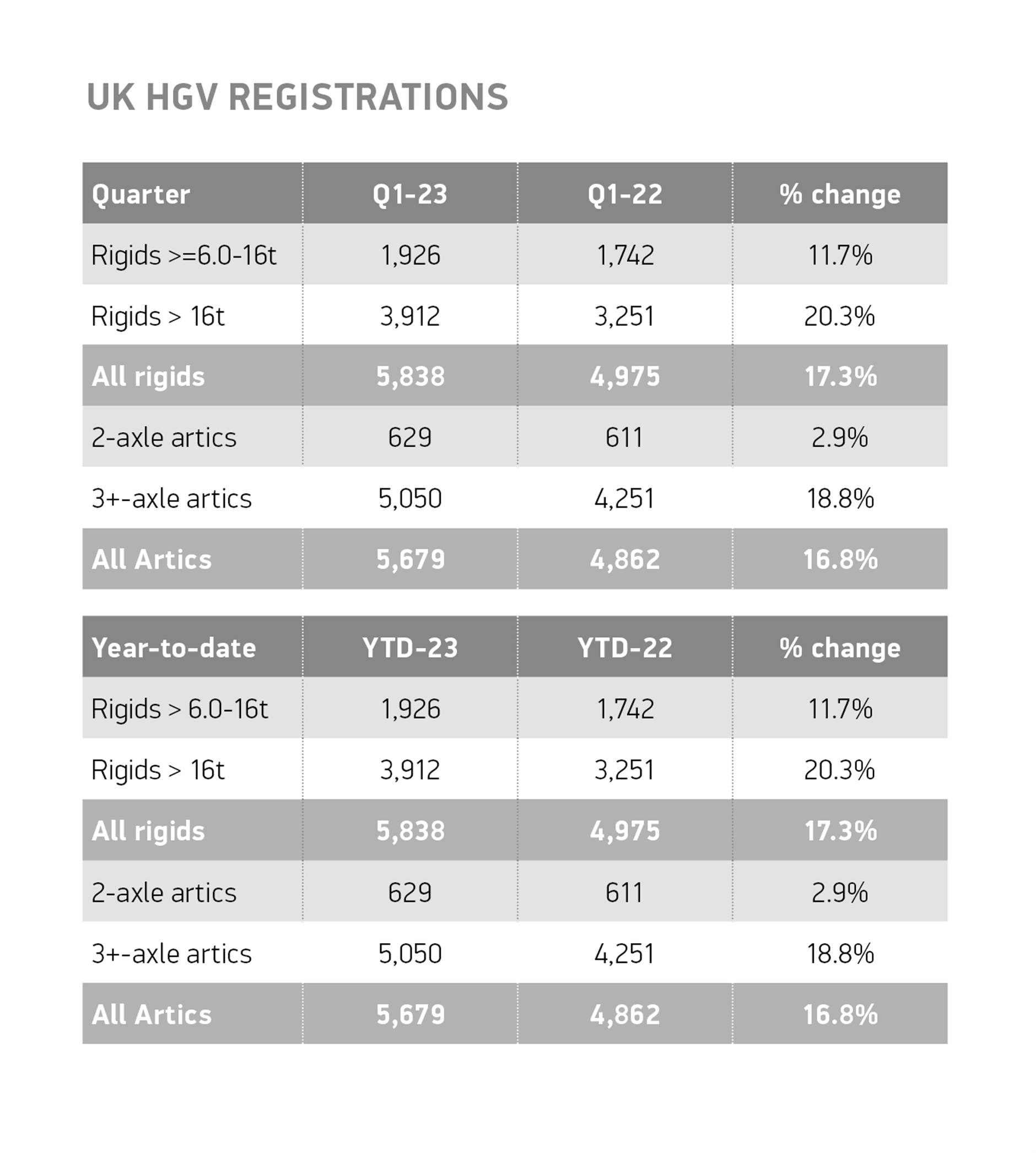

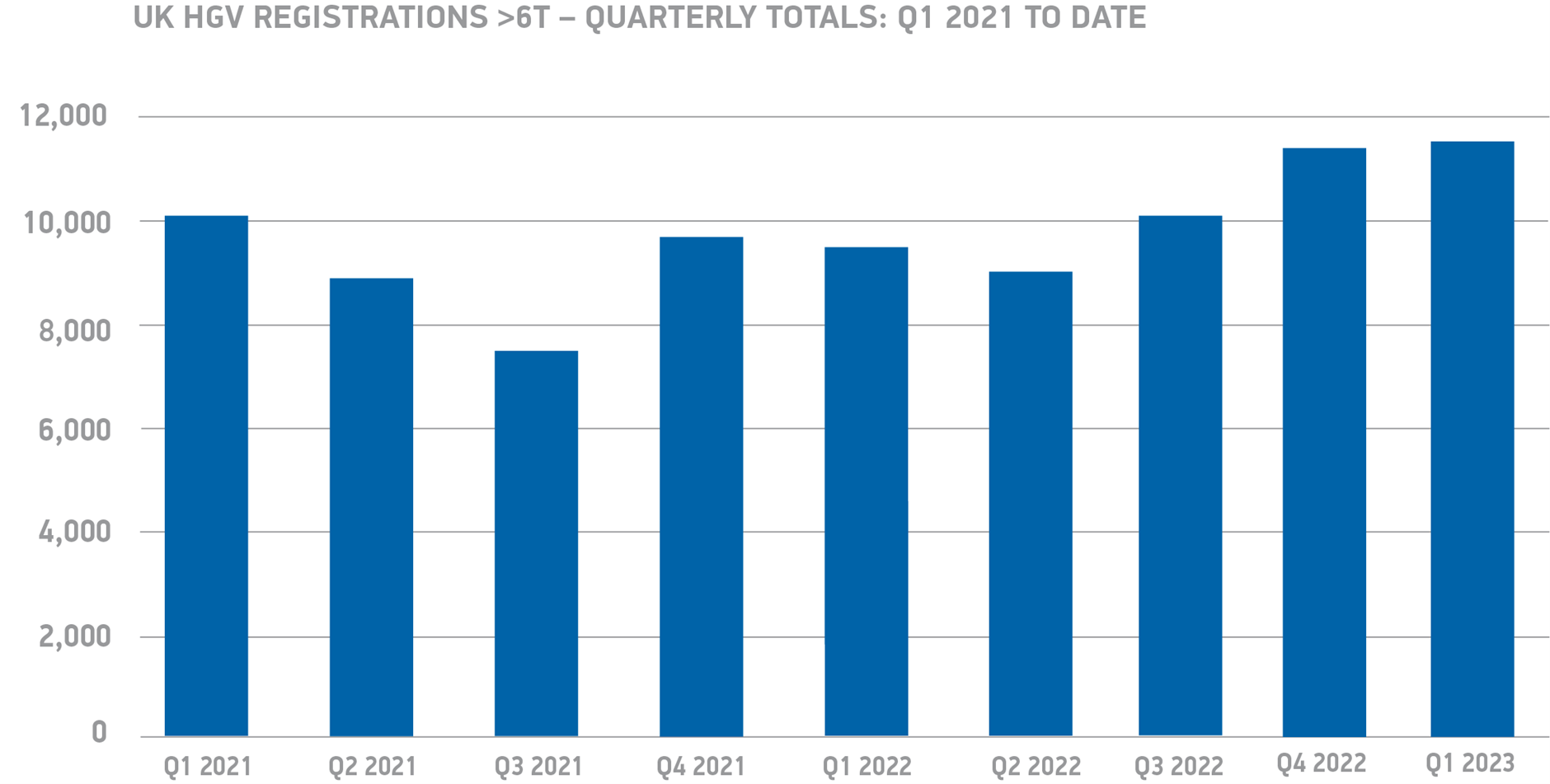

UK demand for heavy goods vehicles (HGVs) grew by 17.1% to 11,517 registrations in the first three months of 2023, according to the latest sales figures from the Society of Motor Manufacturers and Traders (SMMT).

The fourth consecutive quarter of growth, driven by high demand from the haulage, construction and distribution sectors as well as an easing of long-term global supply chain disruptions, means the market is now just 2.9% below Q1 2019.

The rise in registrations was led by double-digit increases of rigids and articulated trucks.

The number of new rigid models joining UK roads rose by 17.3% to 5,838 units, representing the highest Q1 demand for new rigid HGVs since 2019, at 50.7% of all new truck registrations.

Newly registered articulated trucks, meanwhile, rose by 16.8% to 5,679 units.

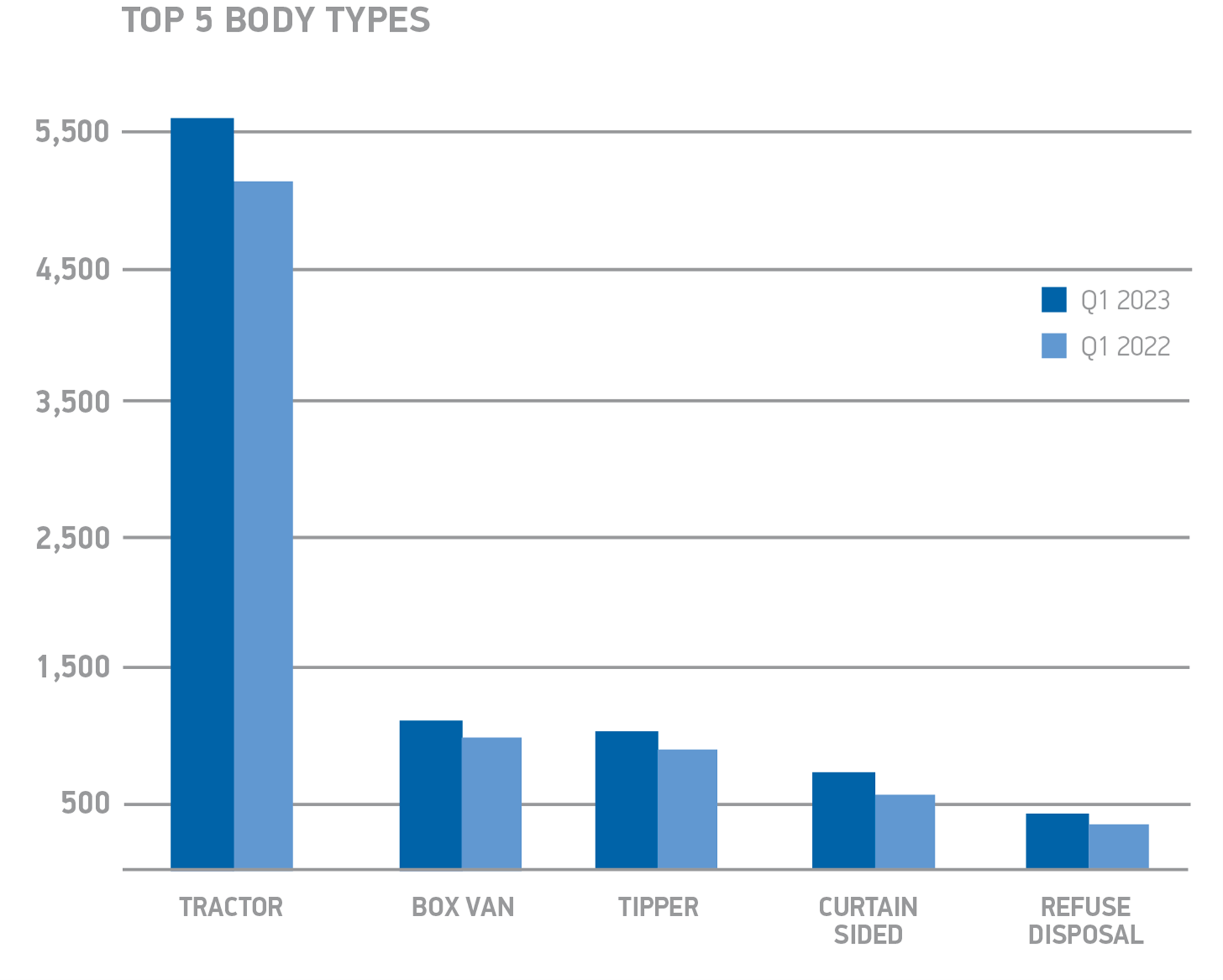

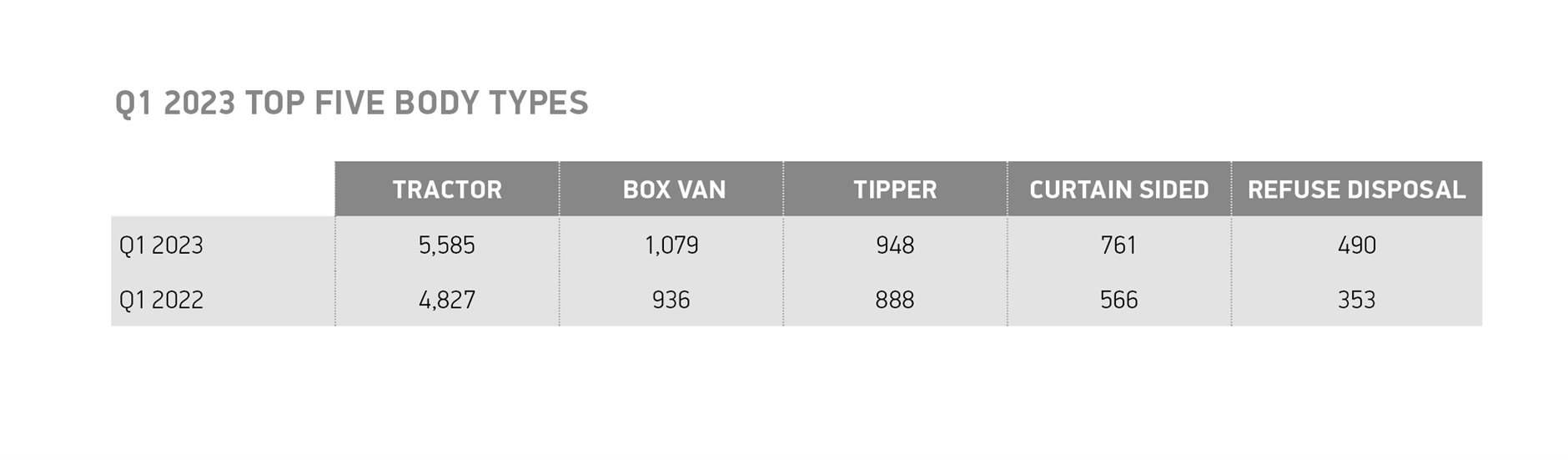

There was a rise in demand for trucks in all major segments, with tractors by far the most popular, up by 15.7% to 5,585 units, while some 1,079 new box vans were registered, up 15.3%.

New registrations of tippers increased by 6.8%, curtainsiders by 34.5% and dropside trucks by 38.8%.

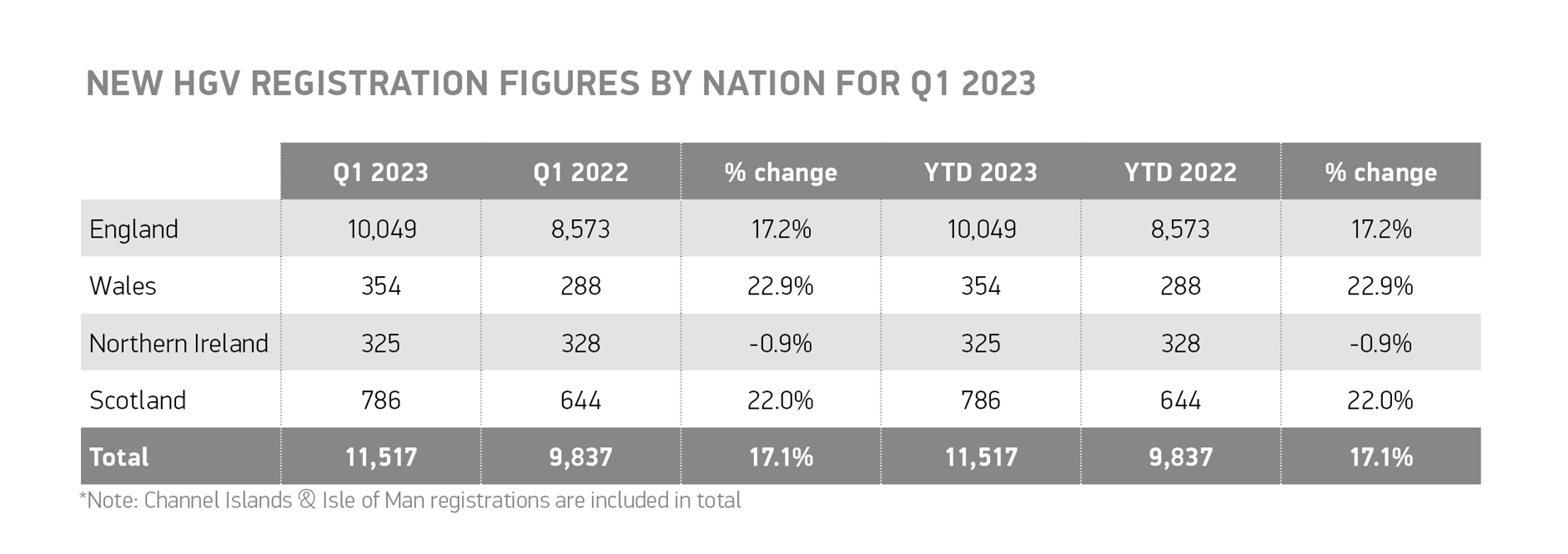

HGV uptake grew across Great Britain, with registrations in England up 17.2%, representing 87.3% of the UK market.

Meanwhile, demand in Scotland and Wales increased by 22% and 22.9% respectively.

South-east England welcomed the most (21%) newly registered HGVs, followed by other key UK logistics regions including the north-west (13.7%) and East Midlands (12.5%).

As truck manufacturers invest heavily to introduce new zero emission vehicles (ZEVs) with 20 models currently available in the UK, the latest electric and hydrogen HGVs represented just 0.3% of the market.

Given the absence of a single HGV-dedicated public charging or hydrogen refuelling station in the UK, and with the sale of new non-ZEV trucks under 26 tonnes due to end in 2035, further measures are needed for operators across the UK to make the switch, says the SMMT.

It is calling on the Government to provide a long-term HGV infrastructure strategy that matches Britain’s world-leading ambitions for truck decarbonisation, delivering sufficient public charging and refuelling points in the right locations, ahead of need.

Globally competitive incentives for the higher cost of ZEV fleet renewal and required depot upgrades is also essential, enabling many operators that naturally face tight margins to commit to the latest high-performing green trucks.

Mike Hawes, SMMT chief executive, said, “The fourth quarter of growth shows that the HGV sector’s recovery from pandemic and supply chain shocks now has momentum.

“For truck fleet renewal to drive UK economic growth and decarbonisation in the long term, however, the zero emission HGV market must gather speed – but operators still need greater certainty that Britain is serious about becoming a globally competitive location for zero emission logistics.

“With an abundance of new electric and hydrogen truck models now ready to join UK roads, a plan is urgently needed to deliver HGV-dedicated public infrastructure, along with incentives for net zero vehicle and depot investments that contend with the world’s major decarbonising nations.”

Mark Main, UK transport lead at EY, says that the HGV market has built on the resilience displayed by the automotive sector in the wake of the pandemic, despite a range of “complex economic headwinds and supply chain constraints”.

“Pre-pandemic annual registrations were 48,535 in 2019, falling to just under 33,000 in 2020,” he added. “This compared to a low point of just over 19,000 vehicles in 2009.

“Annual volumes since the pandemic have increased consistently, rising to 37,163 in 2021 and 40,716 in 2022 – a growth trend currently on track to be emulated in 2023.”

The Fleet News' guide Leadership in fleet is a comprehensive guide on the skills and knowledge you need to become an outstanding fleet leader.

We look at the areas in our sector having the greatest effect on the way fleets operate, offering advice and insight to give fleet decision-makers the confidence to make right decisions and form the best strategies.

Read now

Gareth has more than 20 years’ experience as a journalist having started his career in local newspapers in the 1990s. Prior to joining Fleet News in 2008, he worked in the public sector as a media advisor and is currently news editor at Fleet News.

Login to comment

Comments

No comments have been made yet.